Outwitting fraudsters as they adapt to PSD2 SCA

As the Strong Customer Authentication (SCA) requirement is now enforced across Europe, fraudsters are working harder than ever to adapt—targeting channels and payment methods that are out of scope.

Fortunately, you can be prepared.

In this blog we cover five of the key fraud trends you need to know and how you can tackle them.

Strong Customer Authentication (SCA)

Check out our guide to learn how you can make a smoother transition to SCA—delivering an optimal experience for customers when authentication is required, and minimising the need for SCA challenges.

Outsmart fraudsters in a PSD2 SCA world: How to keep fraud low and convert more orders

Digital disruption is nothing new in eCommerce. But the speed of change is.

In the world of PSD2 SCA, fraudsters are working hard to adapt. They’re adopting new tools, migrating across channels and targetting certain payment methods.

How can your business get ahead?

In this webinar, our experts discuss how you can keep fraud low, convert more orders, and make SCA your competitive advantage.

PSD2 SCA: The 3 things you need to know

In the webinar: Outsmart fraudsters in a PSD2 SCA world, we found three core themes to the questions that were asked by merchants like you.

- How can my business avoid SCA declines?

- How do I optimise SCA exemptions?

- How has fraud shifted since SCA came into force?

Our latest blog summarises the answers to these pressing questions.

Minimise SCA friction

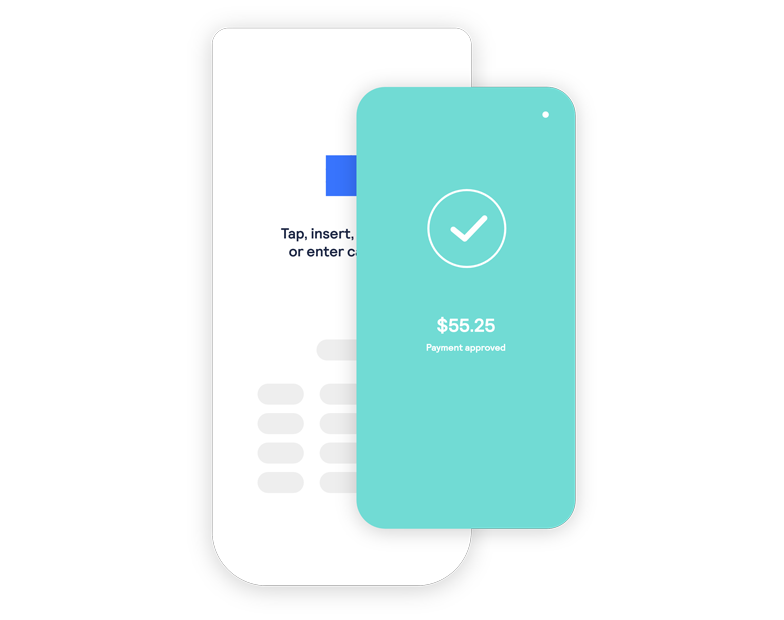

Minimise SCA friction with support for EMV® 3-D Secure (EMV 3DS), the latest 3DS authentication technology designed to deliver frictionless payment authentication across a range of devices.

Minimise SCA challenges

Minimise SCA challenges by recognising and flagging out of scope transactions, and optimising the application of exemptions to reduce the need for SCA challenges.

Deliver the best authentication experience possible

Add 3-D Secure authentication to your fraud management solution to support PSD2 SCA with a seamless customer experience, minimise friction and keep your fraud rates low.

This means:

- Making the SCA authentication process as smooth as possible

- Optimising your SCA exemption strategy—identifying out-of-scope transactions and requesting exemptions where relevant

Find out how Cybersource Decision Manager plus Payer Authentication screens transactions before they are submitted for authorisation—helping you recognise and flag transactions that are out of scope for SCA or may qualify for an SCA exemption.

You don’t have to apply SCA to every transaction, because some transactions are out of scope and others qualify for exemptions. Only applying SCA when you need to will reduce payment friction and lead to better payment experiences.

Cybersource can help you to recognise and flag transactions that are out of scope for SCA—and accurately identify those that qualify for an SCA exemption.

Build rules for transactions that are out of scope for SCA and those that qualify for an SCA exemption

Request exemptions for orders that qualify

Bypass authentication and move straight to authorisation when exemptions are approved

Use business rules to invoke or bypass authentication in ways that comply with PSD2 regulations